While an Advanced Accounting course focuses on financial accounting for corporate mergers and acquisitions, it is important to understand there are many other considerations that go into making a corporate acquisition. Many acquisitions fail because the acquirer (“Acquirer”) does not undertake a panoramic and thorough review of the target company (“Target”) during the due diligence period.

Accountants have a prominent place on the acquisition team. They assist in matters such as due diligence and the review of tax considerations, among others. This article is a survey of the various types of corporate reorganizations contained in Section 368 of the Internal Revenue Code (“IRC”). The term corporate reorganization in Section 368 is a very broad one, including both acquisitions (involving one or more companies) as we would understand them in an accounting sense and reorganizations (involving only one company) as we would commonly understand that term.

Although the form of the acquisition id determined by the corporate attorneys, accountants often have input into this decision. Therefore, an accountant, as a valued business advisor to his client, must be familiar with the various types of corporate reorganizations.

Reorganizations are a very complicated matter under the tax law, and often require the use of experienced tax practitioners (both lawyers an accountants) to craft. The letter of the law must be followed if the parties desire a tax-free acquisition. We will not cover how to fashion a tax-free reorganization in this article, except to note a common requirement of a tax-free acquisition is the Acquirer’s voting common stock be used as consideration in the transaction. Instead, this article will focus on the basic vocabulary of corporate reorganizations.

The types of corporate reorganizations outlined in Section 368 of the IRC are:

Type A Acquisition: The Acquirer purchases the assets and liabilities of the Target. This often is the preferred method of acquiring a company, as any contingent liabilities of Target are left with Target since it retains its corporate existence. Lets take an example. Acquirer is interested in Target, but due diligence reveals Target may have incurred some contingent liabilities yet to be asserted. Acquirer completes the purchase of Target by buying its assets and liabilities. Target still continues to have legal existence, and bears the risk of future contingencies when asserted.

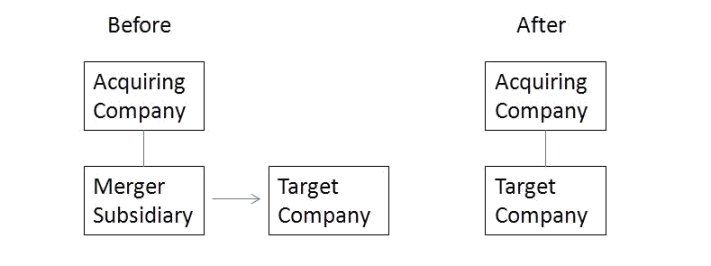

A forward triangular merger is a normal Type A acquisition. It is one answer to the potential contingent liabilities. Acquirer forms a subsidiary, which then completes the acquisition. The assets and liabilities of Target are placed into the subsidiary. Target then goes out of existence. By placing the assets and liabilities of Target into a subsidiary (a legal entity in its own right) Acquiror further insulates itself from acquisition risk at any future claims against the company would generally need to be first asserted against the subsidiary.

A reverse triangular merger is similar to the forward triangular merger except the Target, and not the newly formed subsidiary is the survivor. Target then exchanges its stock for the voting shares of the Acquirer.

Type B Acquisition: The Parent acquires the Subsidiary stock. Sellers usually prefer this method of sale, since the owners of Target sell the entire corporation, including any future contingent liabilities. How do the buyer and seller determine if the acquisition will be a Type A or Type B acquisition? It is simply a matter of negotiation, often coming down to who “wants the deal more.”

Type C Acquisition: This closely resembles a Type A reorganization, with the shareholders of Target receiving stock of Acquirer for the assets of Target. The main difference in the two types of acquisitions is the amount of cash that can by used in the acquisition, and certain liabilities can be excluded from acquisition in a type C reorganization, while not jeopardizing the tax-free nature of the exchange.

Type D Acquisition: These can be “acquisitive D reorganizations” or “divisive D reorganizations”. An example will make an acquisitive D acquisition easier to understand. Acquirer has just completed its acquisition of the assets of Target. Target goes out of business and distributes the stock of Acquiror to its shareholders. An example of a divisive D reorganization is a corporate spin-off. This will be the subject of another article in this series.

Type E Reorganization: This involves only one company, and its outstanding securities are exchanged for the new securities by the company’s shareholders.

Type F Reorganization: This is a mere change in corporate name, state of organization, etc.

Type G Reorganization: This is a restructuring under the protection of the bankruptcy laws. An example is the transfer of assets from one company to another under the protection of the United States Bankruptcy Court.

Some of these reorganizations may seem indistinguishable from others. With practice in this area, a practitioner will develop an expertise. This is a very valuable skill in the accountants’ job market.