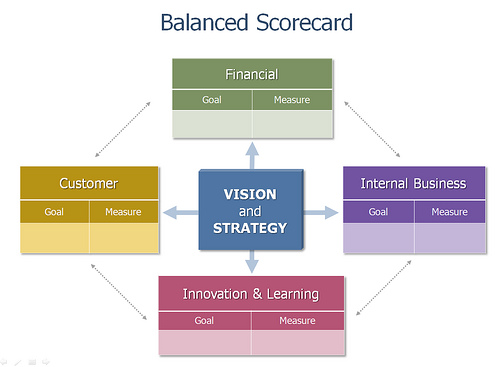

An increasingly popular method of evaluating management performance in the business world is the use of a balanced scorecard. Companies have traditionally used financial measurements as the basis for managerial performance evaluation. For instance, a company CEO would be evaluated using criteria such as EPS, ROI, net income, etc. While these are proper measures of performance for a business, they might not tell the whole story. A balanced scorecard combines financial with non-financial measurements to provide a more complete picture of an organization’s performance. For example, balance scorecards objectives might include non-financial performance objectives for market share, customer satisfaction, and cybersecurity. Recently, balanced scorecards have been expanded to include ESG (environmental, sustainability, and governance) and DEI (diversity, equity, and inclusion) objectives

A balanced scorecard framework takes into account some of the goals might result in trade-offs. This is a major advantage of this system. One example is a company might wish to sacrifice profitability in the short-run to acquire market share. A manager judged only on financial results could conceivably make decisions benefiting the company only in the short run while injuring the company’s long run prospects. This manager may not incur expenses necessary for further market penetration in the future since it will reflect unfavorably on him. A balanced scorecard would take into account the lower reported earnings and reward the manager for achieving his market share objective.

A balanced scorecard approach is an excellent method of evaluating NFP management. Many of the traditional business metrics do not apply in the NFP environment. Factors present in the commercial environment might not be present in the NFP world. Lack of share prices, a profit motive, and open market sales dominate the NFP landscape. To be sure, there are still many financial metrics executive management can be judged by. However, these metrics must be adjusted to reflect the realities of the NFP world. Applicable financial metrics can include solvency ratios such as the current and quick ratios, working capital, attaining a given revenue goal etc.

Financial measures should be supplemented by non-financial metrics on a balanced scorecard. Examples of non-financial metrics useful in the NFP environment are:

- Client satisfaction

- Market penetration

- Number of fundraising events

- Number of client events

- Number of volunteers

- Number of grant applications written

- Number of marketing pieces issued

- Internal control and process improvements

- Number of employees

- Employee satisfaction

This is by no means an exclusive list. The non-financial metrics should be tailored to the activities of the organization and the processes management oversees.

Board members and executive management tend to like the balanced scorecard approach. Once the objectives are agreed to, management knows how it will be evaluated, eliminating unpleasant surprises at review time. A balanced scorecard is also a great timesaver for management as it prepares its reports to the board. Management can design a dashboard report containing monthly data on the objectives enumerated in the balanced scorecard. In the example above, a simple dashboard could contain key financial metrics such as revenue and working capital and non-financial information such as the number of employees, volunteers, grant applications written, etc. The dashboard could be easily set up to display monthly trends. Board members will certainly appreciate the brief description of items they consider key and the trend in these key measures. Of course, there will always be a need for management to provide a narrative in its monthly report. It is difficult, if not impossible to describe contingencies such as a potential lawsuit or a potential opportunity such as a new government program in a dashboard presentation.

An ideal time to implement a balanced scorecard approach is during the budgeting cycle. Realistic metrics are useful for building the budget and the management incentive programs. The budget should result in a small number of key performance indicators (KPIs) that will be included on the balanced scorecard. In short, a balanced scorecard aligns the expectations of the board and management and provides a comprehensive look at the management performance.